China remains the world‘s largest producer of commercial vehicles, construction machinery, and marine vessels, making it the premier global manufacturing hub for multi-cylinder diesel engines. According to the China Internal Combustion Engine Industry Association (CICEIA), total industry sales reached approximately 4.13 million units in 2025, representing a year-on-year growth of 7.35%-7. The commercial vehicle sector was the primary growth driver, with sales reaching 2.04 million units and a growth rate of 10.46%-7.

As the industry faces mounting pressure from new energy alternatives and stringent emission regulations, market concentration continues to intensify, with the top ten players accounting for approximately 78% of total multi-cylinder diesel engine sales. Here is the definitive ranking of China’s top ten diesel engine manufacturers for 2025, based on the latest annual sales data from CICEIA-7.

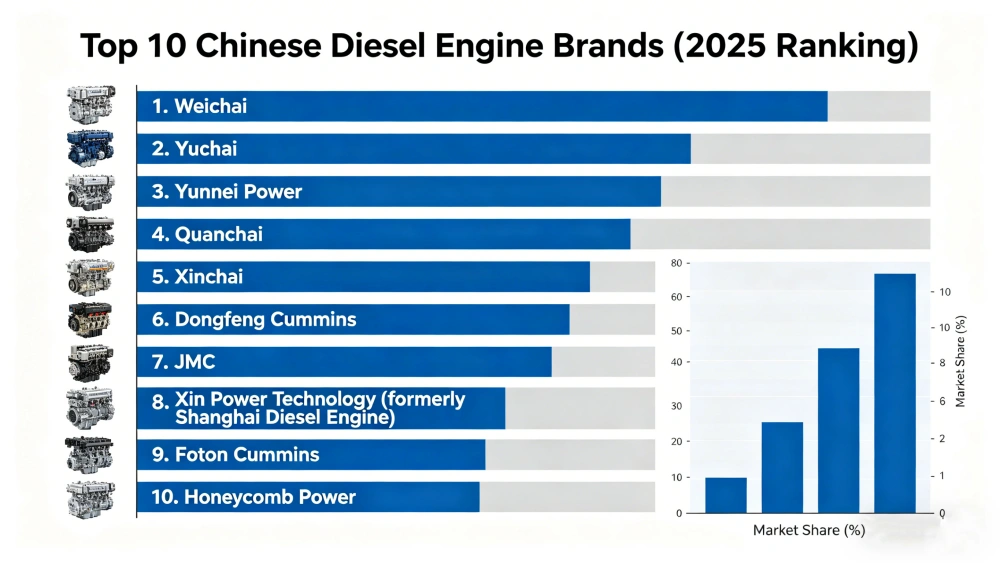

No. 1: Weichai Holding Group

The undisputed leader of China‘s diesel engine market is Weichai Holding Group, headquartered in Weifang, Shandong Province. In 2025, Weichai achieved total sales of 807,300 units, commanding a dominant 19.54% market share-7. This position is further reinforced in the commercial vehicle segment, where Weichai’s cumulative sales reached 469,700 units, representing a 23.02% market share-. The company‘s flagship listed entity, Weichai Power, reported full-year 2025 revenue of RMB 231.8 billion (approximately $32 billion), up 7.5% year-on-year, with net profit attributable to parent company reaching RMB 10.9 billion-. Beyond its core diesel engine business, Weichai has aggressively expanded into high-value segments: its M-series large-bore engines generated RMB 5.81 billion in revenue, growing 65% year-on-year, while data center power generation product sales surged 259% to approximately 1,400 units, fueled by global AI infrastructure demand-. Weichai also leads in thermal efficiency technology, having set a world record of 53% thermal efficiency for diesel engines in 2024-. The group employs over 80,000 people and operates a comprehensive global ecosystem spanning powertrains, commercial vehicles, construction machinery, and new energy technologies.

No. 2: Yuchai Group

Headquartered in Yulin, Guangxi Zhuang Autonomous Region, Yuchai Group secured the runner-up position with 549,100 units sold in 2025, capturing a 13.29% market share-7. Together with Weichai, Yuchai is one of only two manufacturers in the industry to hold a market share exceeding 10%-7. The company demonstrated remarkable growth momentum, with a 23.17% year-on-year increase in sales—the highest growth rate among the top five-9. In the first half of 2025 alone, Yuchai’s engine sales surged 26% year-on-year, significantly outpacing the industry average-. The company achieved double-digit growth across sales revenue, total profit, and engine sales, with its brand value surpassing RMB 114.3 billion, marking 20 consecutive years as the leader in the internal combustion engine industry-. Yuchai has a strong presence in commercial vehicles (with notable growth in tractors, construction trucks, and cargo trucks) and general-purpose machinery, and operates one of China‘s most extensive service and parts networks. The Yuchai Group employs approximately 15,000 people and maintains a vertically integrated production system covering casting, machining, assembly, and testing.

No. 3: Yunnei Power

Based in Kunming, Yunnan Province, Yunnei Power ranked third nationally with 353,700 units sold in 2025, representing an 8.56% market share-7. The company’s sales grew 4.65% year-on-year, maintaining a stable position among the top three-9. However, the company has faced significant financial headwinds in recent years. For the first half of 2025, Yunnei reported revenue of RMB 2.82 billion, a year-on-year decline of 9.85%, and recorded a net loss exceeding RMB 300 million for the first three quarters-. These challenges reflect broader pressures facing traditional diesel engine manufacturers, including accelerating new energy vehicle penetration and intensifying market competition-. Nevertheless, Yunnei’s DEV series diesel engines and DER hybrid engines incorporate internationally advanced technology, meeting China Stage VI emission standards and Phase IV fuel consumption limits, and are widely used across light trucks, medium trucks, light buses, pickups, passenger vehicles, dump trucks, and heavy trucks-. The company has maintained high R&D investment to navigate the industry’s transitional phase, employing approximately 3,000 staff across its operations.

No. 4: Anhui Quanchai

Headquartered in Quanjiao County, Chuzhou, Anhui Province, Quanchai Power sold 334,300 diesel engines in 2025, accounting for an 8.09% market share-7. The company achieved 11.22% year-on-year growth, surpassing the industry average and demonstrating robust operational performance-9. Quanchai has excelled in the agricultural machinery supporting sector, leveraging this niche to drive volume growth. In the first eleven months of 2025, the company sold 307,800 units, a 14.09% increase that outpaced the industry average by 9.16 percentage points-. In the commercial vehicle diesel engine segment specifically, Quanchai recorded 101,200 units sold from January to November, while its third-quarter 2025 revenue grew 9.43% year-on-year-. The company employs around 4,000 people and has built a strong reputation in small-to-medium-bore diesel engines for light-duty commercial vehicles and agricultural applications.

No. 5: Zhejiang Xinchai

Zhejiang Xinchai Co., Ltd., a Shenzhen Stock Exchange-listed company, sold 249,600 diesel engines in 2025, capturing 6.04% of the market-7. The company achieved 2.3% year-on-year growth, maintaining its fifth-place position-9. Xinchai holds a unique competitive advantage as the domestic sales champion for engines used in construction machinery, maintaining a leading position in small-to-medium-bore diesel engines-7. The company’s expertise lies in supplying engines for forklifts, excavators, loaders, and other construction equipment. With a workforce of approximately 3,000 employees, Xinchai has carved out a profitable niche in the construction machinery segment, which remains one of the largest end-markets for diesel engines in China.

No. 6: Dongfeng Cummins (DCEC)

A 50:50 joint venture between Dongfeng Motor Corporation and Cummins Inc. (USA), Dongfeng Cummins Engine Co., Ltd. (DCEC) is the sixth-largest diesel engine manufacturer in China, with total sales of 221,500 units and a 5.36% market share in 2025-7. The joint venture achieved 13.31% year-on-year growth, making it the top-performing joint venture brand in the country-9. DCEC supplies engines for Dongfeng Commercial Vehicles, Chenglong Motors, and other OEMs, with a strong presence in heavy-duty truck applications. In the commercial vehicle multi-cylinder diesel engine segment, DCEC recorded 98,400 units sold in 2025-. The venture employs approximately 2,000 people and benefits from Cummins‘ global technology leadership combined with Dongfeng’s extensive local manufacturing and distribution network.

No. 7: JMC (Jiangling Motors)

Based in Nanchang, Jiangxi Province, JMC (Jiangling Motors Corporation) is a veteran commercial vehicle manufacturer with deep expertise in light trucks, pickups, and light buses-7. In 2025, JMC sold 205,800 diesel engines, holding a 4.98% market share-7. JMC operates as a joint venture between Jiangling Motors Group and Ford Motor Company, leveraging Ford‘s advanced engine technologies for its product lineup. Unlike many other manufacturers on this list, JMC primarily produces engines for captive use in its own commercial vehicles rather than supplying external OEMs. The company employs approximately 20,000 people across its manufacturing and R&D operations, with diesel engines playing a critical role in its light commercial vehicle lineup.

No. 8: New Power Digital Technology (formerly SDEC)

New Power Digital Technology Co., Ltd., part of the SAIC Motor Group and formerly known as Shanghai Diesel Engine Company (SDEC), ranks eighth nationally. The company sold 177,200 units in 2025, capturing 4.29% of the market, with an impressive 24.35% year-on-year growth rate—the highest among the top ten-7-9. As a legacy manufacturer with roots in Shanghai, New Power has successfully transitioned from traditional diesel engines to digitalized power solutions. The company supplies engines for SAIC’s commercial vehicle brands as well as external customers across the truck, bus, construction machinery, and marine sectors. Its rebranding to “New Power Digital Technology” reflects a strategic pivot toward intelligent and new energy power systems, positioning the company for the industry’s long-term transformation.

No. 9: Foton Cummins

Foton Cummins is the second Cummins joint venture to make the top ten list. In 2025, the company completed 171,900 units in sales, with a market share of 4.16%-7-9. The joint venture achieved 8.8% year-on-year growth, demonstrating consistent performance in the heavy-duty engine market-9. Foton Cummins is strategically positioned as the exclusive or primary engine supplier for Foton Motor’s commercial vehicle lineup, including the Auman heavy-duty truck series and the Forland light truck series. The venture has also expanded its customer base to include other commercial vehicle OEMs. Employing approximately 2,500 people, Foton Cummins benefits from Cummins’ global technology platform and Foton’s leadership in China’s commercial vehicle market.

No. 10: Honeycomb Power (Fengchao Power)

Rounding out the top ten is Honeycomb Power (Fengchao Power), a subsidiary of Great Wall Motor, which sold 171,500 units in 2025, holding a market share of approximately 4.15%-9. As the newest entrant to the top ten, Honeycomb Power represents the shifting dynamics of China’s diesel engine landscape. The company has aggressively expanded beyond captive use in Great Wall Motor’s pickup trucks and SUVs to supply external OEM customers. In the first two months of 2026, Honeycomb Power continued to strengthen its market presence, reflecting the brand’s growing competitiveness-. The company’s emergence highlights the trend of automotive OEMs vertically integrating their powertrain production capabilities and competing directly with traditional independent engine manufacturers.

Market Outlook and Industry Trends

China’s diesel engine market is undergoing significant transformation. While total sales reached 4.13 million units in 2025 with 7.35% growth, the industry faces multiple headwinds. Diesel consumption continued its contraction trend in 2025, with apparent consumption declining 2.27% year-on-year to 192.99 million tons, pressured by technological substitution, policy adjustments, and industry restructuring-. Simultaneously, new energy vehicle penetration is accelerating, with the fundamental logic of electric vehicles replacing traditional fuel-powered vehicles remaining intact-.

However, new opportunities are emerging. The AI data center boom is driving unprecedented demand for diesel generator sets. Domestic diesel generator market size reached RMB 12.5 billion in 2025, up 53% year-on-year, with an estimated CAGR of 22% through 2028-. With foreign and joint venture brands currently accounting for 83% of China’s diesel generator market, domestic substitution presents a massive growth runway-.

Industry concentration continues to increase, with the top five players accounting for approximately 72.5% of total sales in early 2026-. As emission regulations tighten and the transition to new energy accelerates, further industry consolidation is inevitable, favoring manufacturers with strong technological capabilities, diversified product portfolios, and financial resilience.